Pension funds face an eternally difficult process of setting goals and then making sure they reach them. It doesn’t sound complicated, but it is.

The better a pension fund can get, though, at setting well thought-out goals, the better chances they have of reaching those goals. Ultimate goals for pension funds often include repairing the pensions deficit, reaching full funding and improving member security. When people’s pensions are on the line, it’s vital that these goals and milestones that come before them are set in a way that’s SMART: Specific, Measurable, Agreed Upon, Realistic and Time-Based:

The acronym SMART has a number of slightly different variations; together, they offer a comprehensive recipe for goal setting:

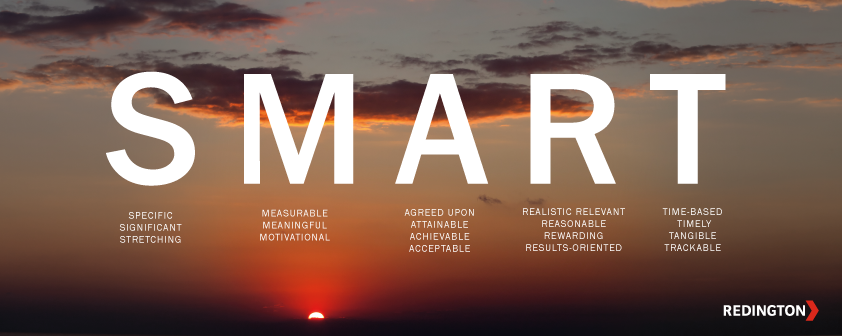

S – Specific. Significant. Stretching.

The goal should be well defined and clear to all the stakeholders, such as the trustees, sponsor, advisors, regulator etc.

M – Measurable. Meaningful. Motivational

All stakeholders should be able to know how the goal is to be achieved, how far away completion is , and recognise when it has been achieved – for example, in the case of pension funds, when full funding has been reached.

A – Agreed upon. Attainable. Achievable. Acceptable. Action-oriented.All stakeholders must agree on the goal. A joint framework is powerful in aligning purpose, and stimulating collective action.

R – Realistic. Relevant. Reasonable. Rewarding. Results-oriented

The goal must be defined within the resources available: time, contributions, risk budget, and governance constraints of the stakeholders.

T – Time-based. Timely. Tangible. Trackable

The goal must work within time constraints in order to create urgency and set a project plan.

If every goal is assessed using this framework and adjusted accordingly to satisfy each requirement, it’s really quite hard not to set robust goals. To quote renowned American philanthropist Elbert Hubbard:

“Many people fail in life, not for lack of ability or brains or even courage, but simply because they have never organised their energies around a goal.”

As we begin to set and implement SMART goals, our clarity of understanding increases. The challenge or problem starts looking less complex, and we begin to see simplicity where before we saw complexity.

In fact, in today’s volatile and uncertain world, there’s a realisation that SMART goals can offer a clear way forward. For pension funds, the SMART approach can be applied to the setting of an investment strategy and the governance that accompanies the implementation of it. The goals are laid out in the form of a Pension Risk Management Framework (PRMF) , for all the stakeholders, trustees, sponsor and advisors to see.

If those goals satisfy the SMART requirements, and are made completely visible, there is a sense of complete accountability, control and transparency. Making decisions suddenly becomes a remarkably easy and fast process. See the example of seamless decision-making based on a clear PRMF in Match.com? Making the pensions and infrastructure romance work

So next time you are setting goals, take this SMART framework with you and require your board to consider it. It will pay off.

Some tips for pension funds on creating SMART goals.

Specific: To set a specific goal, the following questions must be answered:

Who: Who is involved? the Trustees and Sponsor, any other stakeholders?What: What do I want to accomplish? Reach full funding on a Self Sufficiency basis of Gilts + 25bps?When: Establish a time frame. In 10 years’ time?

Which: Identify requirements and constraints. On contributions of £10 million a year and a risk budget of £100 million?Why: Cite specific reasons, purpose or benefits of accomplishing the goal. In order to repair the pensions deficit in an affordable way and improve member security.

A general goal, then, is, “Get to full funding.” But a specific goal is, “Get to full funding, on a self sufficiency basis of Gilts +25bps, in 10 years’ time with a risk budget of £100 million.”

Measurable – Establish concrete criteria for measuring progress toward the attainment of each goal.

When you measure your progress, you stay on track, reach your target dates, and experience the exhilaration of achievement that spurs you on to continued effort required to reach your goal. Measurable goals include, for example, targets for the funding level and the required rate of return needed to reach full funding. See Teresa Ngone’s blog on Finance & Fitness: Get your scheme into shape

Attainable – When you identify crystal clear goals that are most important to you as stakeholders, you begin to prioritise the key investment and risk management decisions to make them happen. Through time, you develop the attitudes, abilities, capability and capacity to reach them. You begin seeing previously overlooked opportunities to bring yourself closer to the achievement of your goals; for example, new investment strategies.

Almost any goal can be reached when steps are planned wisely and time frames for carrying out the goal are established. Goals that may have seemed far away and out of reach eventually become closer and more attainable, not because the goals are easier, but because a group of stakeholders can grow and expand to meet them. The mindset switches from my pension fund will reduce risk OR have long-term investment performance, to my pension fund will reduce risk AND have long-term investment performance. See my blog: the genius of the AND versus the tyranny of the OR

Realistic – To be realistic, a goal must represent an objective towards which both sponsor and trustee are willing and able to work. A goal can be both challenging and realistic; you are the only one who can decide just how challenging your goal should be. But be sure that every goal represents substantial progress. A challenging goal is frequently easier to reach than an easy one because an easy goal exerts low motivational force. A realistic but challenging goal, for example, might be to repair the pension fund deficit AND reduce risk in an affordable manner. That is, de-risk without having to increase deficit repair contributions.

Timely – A goal should be focused within a clear time frame. For pension funds, that might be five, ten or fifteen years. With no time frame tied to a goal, there’s no sense of urgency. If you wanted to lose 10lbs, for example, when do you want to lose it by? “Someday” won’t work. But if you anchor it within a timeframe, “by 31st December”, then you set your unconscious mind into motion to begin working on the goal.

What would it mean if you could repair your deficit in an affordable way by managing risk AND return? When you have a SMART approach, the team of trustees, sponsors and advisors can focus on solving the problem and succeed. A true set of SMART goals leads to better decision making, innovative thinking, the right amount of time focused on the right priorities, better performance and the outcome that matters to you.

Business leaders, Olympic athletes, and leading sports people all know that SMART goals is the key to outstanding success. Let’s put this into practice in pensions and achieve something outstanding.

For more detail please read Alice Cheung’s blog about goal setting Navigating Wonderland and how to capture it in the Pensions Risk Management Framework in the CAPCO Institute Journal of Financial Transformation

One Reply to “Are you SMART? How pension funds can set the right kinds of goals.”

Comments are closed.